I spent most of my career looking for companies that could grow. The pattern was always the same: find a business with room to expand, check if they had the capital to do it, then watch what happened next.

The Small Business Administration’s new “Made in America” loan guarantee program tells me someone in Washington finally figured out the same thing.

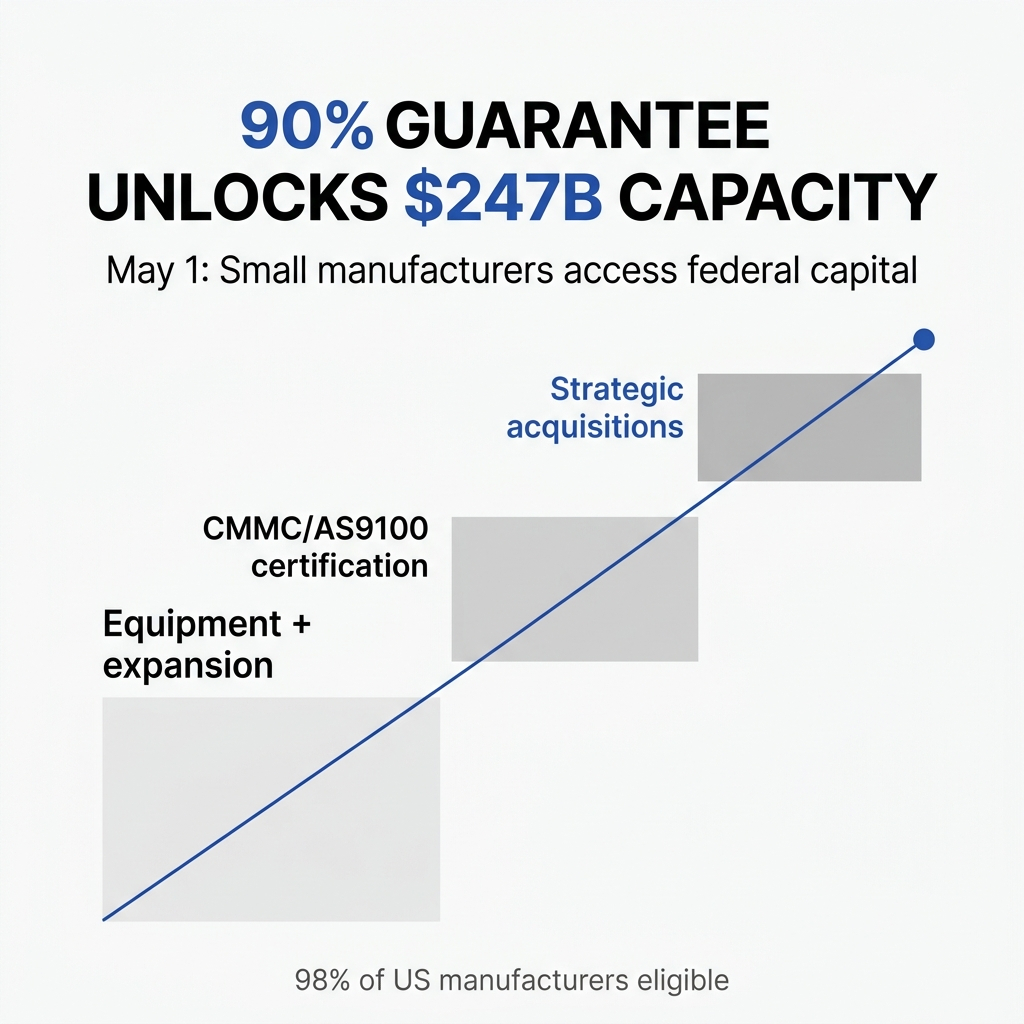

Starting May 1, manufacturers in NAICS sectors 31-33 can access 90% federal loan guarantees. That’s 15 percentage points higher than the standard 7(a) program. The money can fund equipment purchases, facility expansion, inventory, reshoring initiatives, and strategic acquisitions.

This isn’t about tariffs or trade policy. It’s about capital.

The Real Constraint Isn’t Demand

Talk is cheap. Growth is not.

I’ve watched this pattern repeat for decades. A manufacturer has customers lined up. Orders are coming in. The market is there. But they can’t expand because they don’t have the capital to buy the machines, upgrade the facility, or carry the inventory.

The constraint isn’t market demand. It’s access to capital.

Small manufacturers represent 98% of all manufacturers in America. That statistic matters because it means this program could touch nearly every manufacturing business in the country.

Manufacturing capacity utilization sits at 75.6% as of August 2025. The long-run average from 1972-2024 was 78.2%. We have unused capacity, but capital constraints prevent manufacturers from running at full speed or expanding to meet demand.

Even more telling: manufacturing capacity grew at only 0.5% per year from 2022 through 2025. The long-run average is 2% per year. That’s a fourfold difference.

Why 90% Matters

The 90% guarantee does something simple but powerful. It transfers risk from the manufacturer and the lender to the federal government.

When a lender knows the government will cover 90% of a defaulted loan, they’re more willing to approve it. When a manufacturer knows they can get approved, they’re more willing to pursue growth.

This creates a different calculus for expansion decisions.

But here’s what the guarantee doesn’t do: it doesn’t eliminate the need for a solid business case. You still need customers, competitive pricing, and operational efficiency. A 90% guarantee reduces financial risk, but it doesn’t manufacture demand out of thin air.

The economics still have to work.

The Hidden Barriers Nobody Talks About

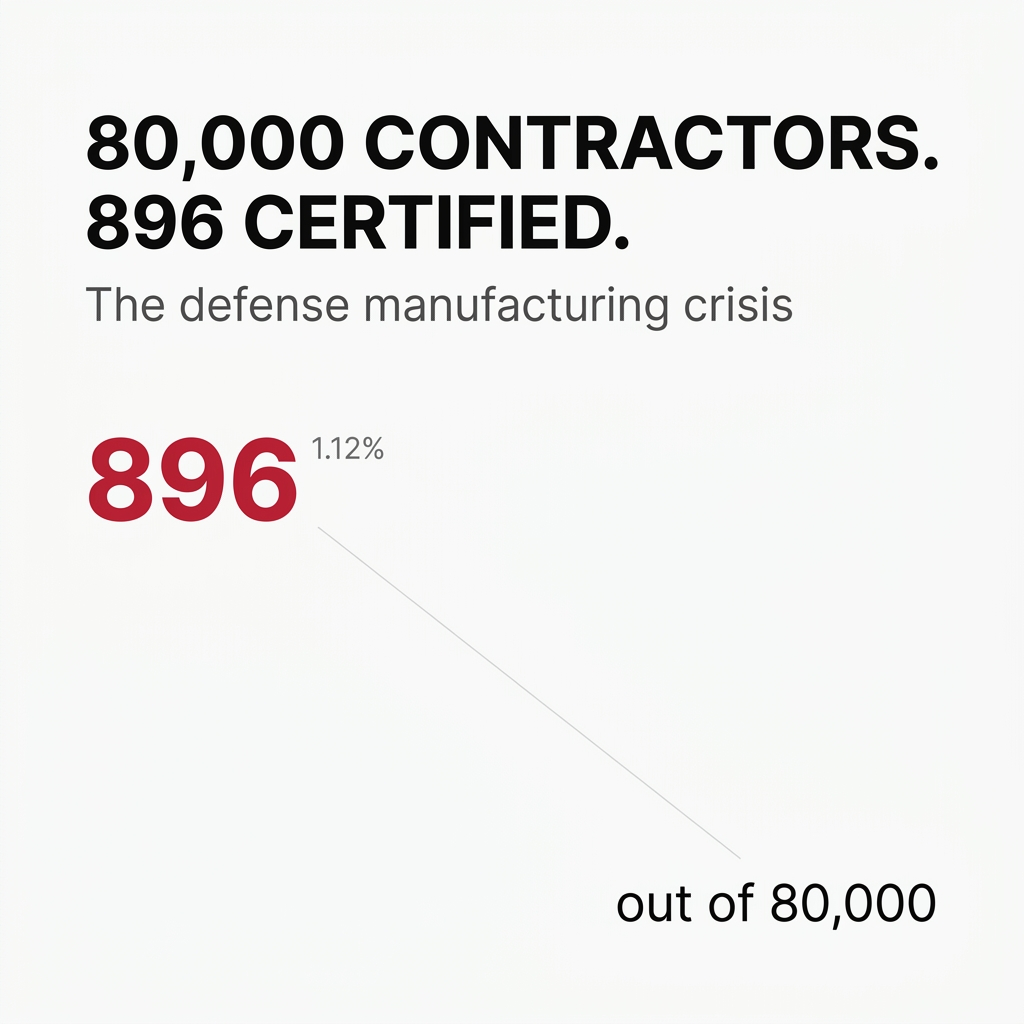

Equipment costs are obvious. What’s less obvious are the certification barriers that keep manufacturers from accessing high-value contracts.

Defense contractors face over $100,000 to achieve CMMC Level 2 certification. AS9100 aerospace certification adds another $20,000 to $45,000 for small shops. These aren’t optional expenses. They’re market entry requirements.

You need capital before you can even bid on the work.

This creates a catch-22. Manufacturers need the certification to win contracts. They need contracts to justify the certification investment. The 90% guarantee could break that cycle by funding pre-revenue compliance investments.

But certification is just one piece. Modern manufacturing requires digital infrastructure, security systems, and IT capabilities that compound capital requirements beyond traditional equipment purchases.

Strategic Acquisitions Change the Game

Including acquisitions in eligible uses signals something important. The government recognizes that manufacturing reindustrialization might require industry consolidation, not just organic growth.

This creates pathways for capable operators to absorb struggling facilities, acquire complementary capabilities, or achieve economies of scale.

I’ve seen this pattern before in other industries. Sometimes the fastest way to build capacity isn’t to build from scratch. It’s to buy an existing operation and improve it.

The acquisition provision could accelerate consolidation in fragmented manufacturing sectors where scale matters.

The Infrastructure Gap

Capital access solves one problem. Deployment capacity solves another.

The Manufacturing Extension Partnership (MEP) network provides operational consulting, technical assistance, and financial guidance. It helps small manufacturers deploy capital effectively.

You can have all the capital in the world, but if you don’t know how to implement automation systems, navigate compliance requirements, or optimize production processes, that capital won’t generate returns.

This is where policy coordination matters. Launching a loan guarantee program while cutting MEP network funding creates an incomplete solution. It’s like providing building materials without architects or engineers.

What This Means for Manufacturing

Nearly 500,000 manufacturing jobs remain unfilled due to skills mismatch. Companies announced $1.7 trillion in new manufacturing investments, but much of that exists in planning documents rather than operational capacity.

The gap between announced intentions and deployed capital is massive.

This loan program addresses one constraint: capital access. But manufacturing expansion requires simultaneous investment in workforce development, technical support infrastructure, and digital transformation capabilities.

For every dollar spent in manufacturing, there’s a $2.65 total impact to the U.S. economy. For every manufacturing worker, 4.8 workers are added to the overall economy. Manufacturing has one of the largest sectoral multipliers.

That means manufacturing investment creates broader economic effects than most other sectors.

The Risk Transfer Question

By reducing downside risk through 90% guarantees, the program effectively transfers risk from private decision-makers to taxpayers.

This could encourage necessary but risky bets on capacity expansion. Or it could create moral hazard where operators pursue marginal projects they wouldn’t self-finance.

The difference comes down to whether “leaders willing to bet on the future” means visionary entrepreneurs or opportunistic risk-takers exploiting subsidized capital.

Time will tell which group shows up.

What I’m Watching

The program launches May 1. I’m interested in three things:

First, uptake rates. How many manufacturers actually apply and receive funding? Strong demand signals that capital constraints were real. Weak demand suggests other barriers matter more.

Second, deployment patterns. What do manufacturers buy? Equipment purchases tell one story. Certification investments tell another. Acquisitions tell a third.

Third, coordination with support infrastructure. Does MEP network funding increase to match the new capital availability? Or does policy fragmentation continue?

The effectiveness of this program depends on ecosystem coordination. Capital access matters, but it’s not sufficient by itself.

Manufacturing reindustrialization requires more than financial engineering. It requires workforce development, technical support, and infrastructure investment working in concert.

But you have to start somewhere. Capital access is a reasonable place to begin.

Leave a comment